Common bookkeeping mistakes are errors made while recording or categorizing business transactions. These mistakes distort financial reports and lead to inaccurate profit or tax figures.

Do you think when bookkeeping goes wrong, it just messes up your spreadsheets? Nope! It shakes up entire businesses.

- In 2014, Bank of America overstated its capital by $4 billion due to a simple accounting error.

- In 2017, Uber miscalculated driver commissions, which cost New York drivers tens of millions.

And these weren’t startups with shoestring budgets. They were giants! Yet their stories show how small bookkeeping mistakes can become major financial and reputational damage.

Don’t want this? Read this article to know about the twelve common bookkeeping mistakes most new business owners make (along with their easy fixes).

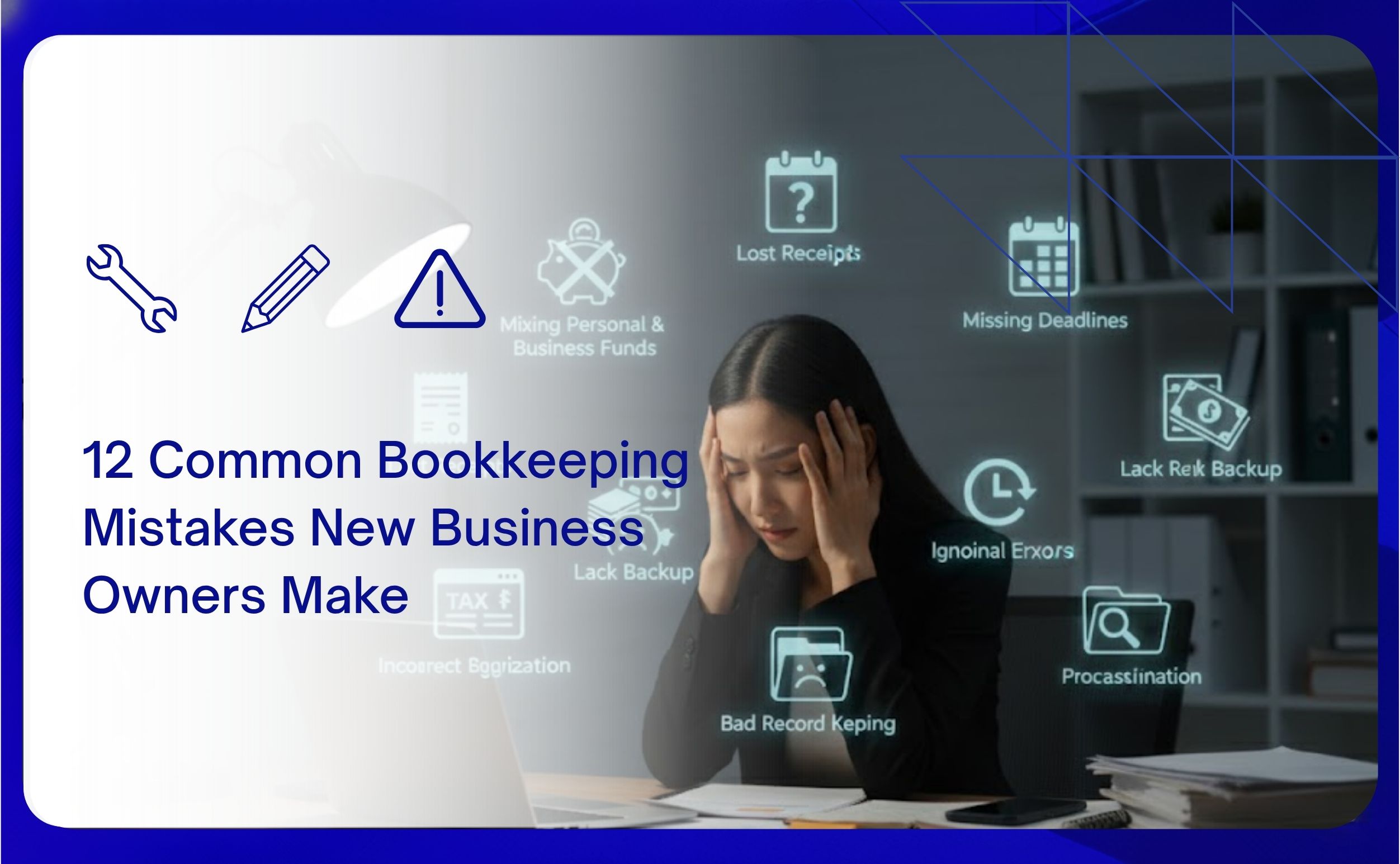

12 Common Bookkeeping Mistakes You Must Avoid in 2025!

Studies show that U.S. businesses lose an estimated $7.8 billion annually due to accounting errors and manual financial reporting issues. Particularly, small and medium-sized businesses (SMBs) are vulnerable as their accounting errors lead to penalties, wasted resources, and higher audit risks.

Don’t want to bear all this? Below are twelve common bookkeeping mistakes you must avoid in 2025:

1. Mixing Personal and Business Expenses

Do you pay for a client lunch with your personal card and buy groceries with your business account? – These practices confuse bookkeepers! Such mixing of personal and business expenses leads to the creation of inaccurate financial statements. Additionally, it creates legal risks, particularly during audits or lawsuits.

Need a fix? Always keep your dedicated business bank and credit accounts separate. Mark your business cards to avoid confusion + keep a small cash reserve for business-only use. If you ever mix expenses by mistake, reimburse the relevant account.

2. Ignoring Your Financial Statements

Every business prepares these three major financial statements:

- Income statement

- Balance sheet

- Cash flow

They show exactly how your business is performing. If you don’t review them, you’re operating blind. As a VP, director, or senior manager of a growing D2C company, you must analyse these reports to:

- Manage cash flow

- Plan budgets

- Identify tax deductions

- Track profits

Additionally, they also strengthen your loan or investor applications by proving financial stability. Thus, always make it a habit to read your statements periodically (say every quarter).

3. Losing or Throwing Away Receipts

Receipts are your proof of business spending! Without them, you can’t justify deductions if the tax department audits your return. Lost receipts can also lead to penalties or rejected tax claims. Thus, the best approach is to store all receipts (even digital copies are completely acceptable).

As a pro tip, keep them for at least seven years. Record basic details like the date, vendor, and purpose of each expense.

4. Counting Internal Transfers as Income

If your business uses more than one account (say PayPal, Stripe, or a foreign currency account), you’ll usually move money between them. Now, the bookkeeping mistake here is, your accounting software might see these transfers as new income instead of money moved within your business. This mistake inflates both your income and profit.

Thus, each time you transfer money, update the entry to show it as a “transfer,” not “income.” Doing this keeps your books accurate and prevents you from overpaying taxes.

5. Ignoring Sales Tax Rules

Sales tax isn’t optional! The tax office won’t overlook mistakes just because you didn’t know the rules. Every business has a legal duty to collect and pay sales tax correctly. Failing to do is a common bookkeeping mistake that results in heavy penalties as follows:

| Type of Penalty | Description | Rate / Amount | Maximum Limit / Notes |

| Failure to Pay Tax | Charged when you file your return but don’t pay the full tax owed by the due date. | 0.5% of unpaid tax per month (or part of a month). | Capped at 25% of the unpaid tax. |

| Accuracy Related Penalty | Applied when underpayment is due to:

|

20% of the underpaid amount. | Applies only to the portion of tax underpaid. |

| Civil Fraud Penalty | Imposed if underpayment is due to intentional fraud or deliberate misrepresentation. | 75% of the portion of the tax is underpaid due to fraud. | It can be applied in addition to other penalties. |

| Interest on Unpaid Taxes and Penalties | Accrues daily on unpaid tax and penalties until full payment. | Interest rate set quarterly (federal short-term rate + 3%). | Continues until all dues are paid. |

To avoid these penalties, you can outsource your bookkeeping department to leading US accounting firms, like Atidiv. Their CPAs can let you determine:

- What taxes apply to your products or services

- When to collect them

- How to file them on time

6. Misclassifying Workers

Employees work under your direction and are usually on the payroll. In contrast, contractors work independently and handle their own taxes. The IRS takes this distinction seriously because misclassifying workers can result in unpaid employment taxes (that can again attract fines and penalties).

For more clarity, let’s understand in detail why you must properly classify your staff:

- Employment Taxes are at Stake:

- When someone is classified as an employee, the employer must withhold the following from their paycheck:

- Income tax

- Social Security

- Medicare contributions

- Also, they must pay the employer’s share of those taxes.

- If a worker is wrongly labeled as a contractor, none of this happens, and the IRS loses that tax revenue.

- When someone is classified as an employee, the employer must withhold the following from their paycheck:

- Protecting Worker Rights and Benefits:

- Employees are legally entitled to benefits such as unemployment insurance and workers’ compensation.

- Misclassifying them as contractors can deny these protections and shift the financial risk to the worker.

- Preventing Deliberate Tax Avoidance:

- Some businesses misclassify workers on purpose to reduce costs.

- By doing so, they try to avoid:

- Payroll taxes

- Benefit contributions

- Administrative duties

- The IRS monitors this closely to prevent abuse and make sure there is fair competition among businesses.

Thus, you should always verify each worker’s status before hiring. If you need bookkeeping help for your small business, you can even use the services of third-party agencies.

7. Hiring the Wrong Bookkeeper for the Job

Cheap bookkeeping may sound like a win! But it often costs more in the long run. An inexperienced bookkeeper can make several basic bookkeeping mistakes, such as:

- Misclassifying expenses by recording costs under the wrong category.

- Missing tax deductions that could reduce your tax bill.

- Failing to reconcile accounts

- Recording revenue incorrectly, such as counting income twice or in the wrong period

- Ignoring compliance deadlines and exposing your business to penalties.

Thus, it is always better to hire experienced bookkeepers who know which expenses are deductible, how to structure your accounts, and how to keep your records organized.

8. Skipping a CPA When You Need One

A Certified Public Accountant (CPA) is more than a tax preparer! They let you:

- Identify tax deductions

- Plan year-end strategies

- Manage sales tax

Additionally, they also represent you during an audit or tax scrutiny. If you’re a growing D2C company earning $5M+ revenue, you should consider outsourcing your accounting functions to third-party firms instead of hiring CPAs internally.

With Atidiv, you get access to a network of 390,000+ chartered accountants and CPAs. Our past clients have also achieved cost savings of up to 60% as compared to running in-house accounting teams. Book a free consultation to learn more!

9. Recording Owner Payments as Business Expenses

If you’re a sole proprietor or run a single-member LLC, the money you take out of the business is not an expense. Many owners make this common bookkeeping mistake and end up lowering their reported profit unintentionally.

Please note that these payments should be recorded as “Owner’s Draw”. This category represents the money you’ve taken out for personal use. Always remember that expenses belong to the business and draws belong to you!

10. Guessing How to Manage Your Books

Many new business owners of D2C companies start by:

- Recording numbers

- Picking categories that “look right”

- Hoping everything balances out at the end of the year

This is a wrong approach and a common bookkeeping mistake! Usually, when tax time comes, such leaders realize their entire year’s records are off due to:

- Wrong expense categories

- Missed deductions

- Inaccurate revenue recognition, and more

All this delays return filings and attracts heavy penalties. Thus, you should always hire agencies, like Atidiv, that specialize in bookkeeping for small business owners. Our expert team prepares accurate records from day one!

11. Using a One-Size-Fits-All System

Every business has its own kind of income, expenses, and reporting needs. If your bookkeeping setup isn’t designed for your business, your prepared books of accounts will never give a true and fair view.

The fix? You should create a custom chart of accounts. It’s a list of all the categories you use to record income, expenses, assets, and liabilities. When customized for your business, it offers the following advantages:

- You can track income and spending by type, like sales, rent, supplies, or marketing.

- Proper categories allow you to identify deductible expenses and avoid missing claims.

- You can compare month-on-month data and spot trends (say changes in income or costs).

A professional bookkeeper or accountant can set this up. Firstly, they review your business model, income sources, and expenses. Next, they build account categories that match your operations.

12. Waiting Until the Guilt Kicks In

Several senior managers of D2C companies delay bookkeeping! They wait until the receipts pile up and then can’t remember what half of them were for. Please realize that when you postpone bookkeeping for months, you risk:

- Forgetting key details

- Missing deductions

- Working with outdated numbers

The impact? Your business decisions will be based on old or incomplete data. Thus, always start bookkeeping as the financial year begins and reconcile your accounts at least once a month.

8 Accounting Tips for Small Business Owners!

- Separate personal and business finances. Keep accounts and cards distinct to avoid confusion and legal issues.

- Track every expense for accurate reporting and maximizing tax deductions.

- Reconcile accounts regularly. Match bank statements with your books to catch errors early.

- Use a custom chart of accounts to better organize income and expenses.

- Keep digital records by scanning invoices and receipts.

- Monitor cash flow weekly.

- Invest in accounting software to automate calculations, financial reporting, and tax filings.

- To save costs and gain access to professional expertise from day 1, hire accounting outsourcing companies.

Searching for a Bookkeeping Partner? Hire Atidiv in 2025! We have a 95% Client Retention Ratio..

Till now, you must have understood that some common bookkeeping mistakes can result in heavy penalties from government authorities like the IRS. These mistakes are mostly related to:

- Mixing personal and business finances

- Misclassifying workers incorrectly

- Ignoring sales tax obligations

- Recording owner payments as expenses

- Losing or misplacing receipts

Please understand that bookkeeping is a complex process! Your books must comply with established accounting standards and laws, such as:

- IFRS (International Financial Reporting Standards)

- GAAP (Generally Accepted Accounting Principles)

- Federal and state tax regulations

Due to strict compliance requirements, several growing D2C companies and consumer brands suffer legally! In 2025, to avoid the hassle, many SMBs are now delegating bookkeeping work to leading U.S. accounting firms.

Partner With Atidiv in 2025!

If you are looking for accounting outsourcing companies, Atidiv is a top firm with 16+ years of experience. Recently, Atidiv partnered with a NYC-based start-up and worked on their finance and accounting operations. We addressed issues in:

- Bookkeeping

- Inventory accounting

- Cash-flow management

Our expert team helped the company achieve faster monthly closures. This resulted in 80% time savings + a 50% reduction in costs! Need similar results? Book a free consultation call to learn how we can help you.

Common Bookkeeping Mistakes FAQs

1. How to balance books for a small business?

Balancing the books means making sure your business records match your actual bank balances. Let’s see how it’s done step-by-step:

- Record all transactions: Enter every sale, expense, and payment in your accounting software.

- Reconcile bank accounts: Match each transaction in your books with your bank statements.

- Categorize correctly: Assign income, expenses, and transfers to the right accounts.

- Check trial balance: Make sure your total debits equal total credits.

- Review financial reports: Generate balance sheets and profit and loss statements to confirm accuracy.

Lastly, if there are any discrepancies, trace them back to the source (missing receipts, duplicate entries, or incorrect postings).

2. What happens if I miss filing sales tax in 2025?

Missing or underpaying sales tax can lead to heavy penalties from the IRS and state tax authorities. You may be charged interest and asked to pay fines up to 25% of the unpaid tax.

3. Why is cheap bookkeeping risky?

Low-cost or inexperienced bookkeepers often:

- Misclassify transactions

- Miss tax deductions

- Record revenue under the wrong heads

These small errors delay return filings and may attract notices. Thus, you should always invest in skilled bookkeeping. This can be easily done by outsourcing your accounting operations to leading agencies, like Atidiv.

4. How do I avoid misclassifying employees and contractors?

To make appropriate classifications, you must follow IRS guidelines! Always remember that employees work under your control, while contractors operate independently. Some other key distinctions the IRS considers are:

- Behavioral Control: If you decide how, when, and where the worker does the job, they’re likely to be an employee. Contractors decide their own methods.

- Financial Control: Employees are paid a regular wage or salary, while contractors invoice for specific projects and can make a profit or loss.

- Tools and Expenses: Employees usually use company tools and get reimbursed for expenses. In contrast, contractors bring their own tools and bear their own costs.

- Relationship Type: Employees often receive benefits like health insurance or paid leave, while contractors do not.

Misclassification can trigger unpaid payroll taxes, penalties, and audits!